Table of Content

- Why Most Next Best Offer Strategies Stall at Segmentation

- What Real-Time Decisioning Actually Means for Banks

- The Four Layers That Make It Work

- What This Looks Like in Practice

- The Organizational Capability That Banks Underestimate

- The Difference Between Knowing and Acting

- How evamX Powers Next Best Offer in Banking

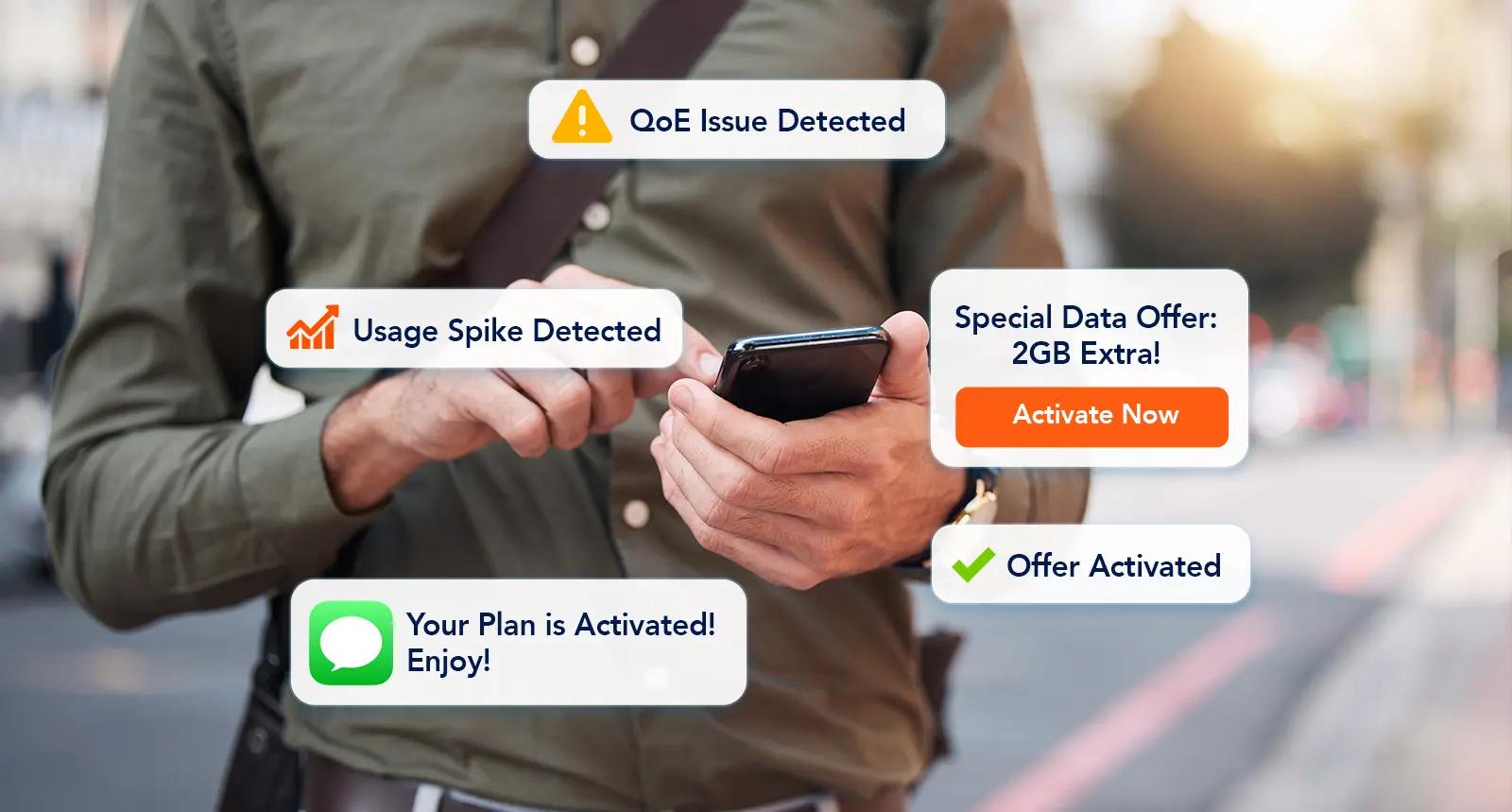

A customer declines an auto loan offer at the ATM. Moments later, they log into the mobile app and the same offer appears again.

The customer ignores it. The bank has wasted two inbound moments, learned nothing from the first rejection, and signaled to the customer that the system does not actually know them.

This is not a targeting problem. The bank had the customer's attention twice. It is an orchestration problem, and it is the most common failure mode in how banks implement next best offer today.

Why Most Next Best Offer Strategies Stall at Segmentation

The premise of next best offer is straightforward: understand the customer, predict what they need, and present the right offer at the right moment. Every bank investing in this capability understands the logic. The gap between logic and execution is where most implementations break down.

The root cause is architectural. Most next best offer strategies are built on segmentation and batch campaign logic. A cohort of customers is identified as eligible for a product, a message is crafted, and a campaign is scheduled. By the time it reaches the customer, the context has already shifted. The customer who was browsing loan calculators at 9 AM receives a loan offer push notification at 6 PM, eight hours after the intent signal fired, long after the decision window has closed.

Worse, each channel in this architecture operates independently. The ATM system runs its own offer logic. The mobile app has a separate campaign layer. The call center agent sees a different CRM view. When a customer declines an offer on one channel, that signal is rarely transmitted to the others in real time. The result is repetition, inconsistency, and the steady erosion of customer trust that comes from feeling like the bank is broadcasting to a segment rather than engaging with a person.

The intelligence in these systems is often sophisticated. The execution layer is where the value leaks out.

What Real-Time Decisioning Actually Means for Banks

Genuine next best offer decisioning is not a faster version of campaign scheduling. It is a different architecture entirely, one where the offer decision is made at the moment of the customer interaction, not in advance.

When a customer logs into mobile banking, makes a transaction, visits a product page, or calls the contact center, that interaction generates an event. In a real-time decisioning architecture, that event is the trigger. The system evaluates it immediately against the customer's full context: their product holdings, transaction history, recent behavior, active offers, previous responses, and predictive model outputs. The most relevant action is determined in milliseconds.

The decision is not retrieved from a pre-computed segment. It is made live, on current data, in the moment the customer is present. This distinction matters more than it might appear. A customer whose salary just landed in their account is in a different decisioning context than the same customer three days earlier. A customer who just failed a transaction is in a different state than one who completed a purchase successfully. Segment-based logic cannot capture these differences. Event-driven decisioning is built around them.

The Four Layers That Make It Work

For bank technology and marketing leaders evaluating how to implement next best offer effectively, the architecture question is more important than the vendor feature list. There are four layers that determine whether the system delivers on its promise.

The first is event capture. The system must receive signals from every relevant source, including core banking, card systems, mobile and web apps, ATM and kiosk networks, IVR and call center platforms, and CRM, as they occur, without batch lag and without data duplication. A zero-copy streaming architecture means the decisioning layer is always working with current data, not a stale extract from last night's warehouse job.

The second is eligibility and suppression logic. Before any offer is presented, the system checks whether the customer qualifies for it based on live profile data, and whether any suppression rules apply: a prior rejection, a cooling-off window, an active complaint, or a concurrent journey that would make this offer inappropriate. This layer is what prevents the ATM rejection from repeating on mobile. It is also what ensures that a customer in a service recovery journey does not simultaneously receive a promotional message that would undermine both interactions.

The third is priority scoring. When multiple offers are eligible for a customer at a given moment, the system ranks them based on a combination of business priority, predicted customer propensity, and contextual relevance. The output is a single ranked decision: the next best offer for this customer, in this channel, at this moment. Not the best offer from last week's segment. The best offer right now.

The fourth is omnichannel execution. The decision is delivered through whatever channel the customer is currently using: in-app notification, ATM screen, mobile push, email, SMS, WhatsApp, or agent screen, from a single orchestration layer. When the customer responds, that response is reflected across all channels immediately. A conversion closes the offer in every pending queue. A rejection suppresses it everywhere.

What This Looks Like in Practice

The scenarios where real-time next best offer decisioning delivers the most measurable impact in banking share a common characteristic: there is a narrow window of customer intent that closes quickly, and the value of the interaction is determined by whether the system can act within that window.

A customer visits the loan calculator in the mobile banking app, inputs their desired amount, and then navigates away without applying. This behavior is a high-intent signal. A real-time system detects it as it happens, checks the customer's pre-approval eligibility against live data, and surfaces a personalized loan offer within the same session, while the intent is still active. The same offer delivered via a scheduled campaign the following Tuesday converts at a fraction of the rate, because the customer has moved on.

A customer attempts a card payment at an online merchant and the transaction is declined, not because of insufficient funds, but because online transactions are disabled on their card by default. In a traditional system, this event is logged, the customer calls the contact center, and the issue is resolved with friction and cost. In a real-time decisioning architecture, the system detects the declined transaction instantly, identifies the cause, and delivers an in-app message guiding the customer to enable online transactions with a single tap, before frustration sets in and before a competitor's card becomes the default.

A high-value customer initiates a large transfer to an external account. At the moment they reach the confirmation screen, before the tap that sends the money out, the system presents a contextual savings offer: a rate that makes keeping the balance more attractive, with a one-tap account opening flow. The customer retains full choice. But the offer is there at the exact moment of the decision, not in a weekly email digest that arrives after the money has already left.

A customer registers their debit card with a third-party payment app and the first transaction is declined due to merchant category restrictions. Rather than losing this customer to a competitor card, the system detects the event, identifies the restriction as the cause, and sends an immediate in-app message that resolves the issue before the customer closes the app. Every subsequent payment through that app stays on this card, not a competitor's.

In each of these scenarios, the offer itself is not exceptional. What is exceptional is the timing: the system's ability to detect the moment and respond within it.

The Organizational Capability That Banks Underestimate

There is a second dimension of next best offer implementation that receives less attention than the technical architecture but has an equally significant impact on outcomes: who controls the decisioning logic.

In most bank environments, modifying an offer eligibility rule, adding a new suppression condition, changing a priority score, or activating a new display zone requires a development ticket, a testing cycle, and a deployment window. The marketing or CVM team that owns customer engagement cannot act at the pace customer behavior changes. By the time a new offer logic is live, the market condition that prompted it has often passed.

Effective next best offer at scale requires that business users, the teams who understand customer needs and product strategy, can configure and modify offer logic directly, without IT dependency. This means eligibility rules built in a UI rather than code. Suppression windows set by the marketing team rather than a developer. New channels and display zones activated by business configuration rather than engineering work. Offer simulations run in real time before go-live, so the team can validate who will see what before activating.

This capability does not reduce the role of technology teams. It removes the bottleneck that prevents marketing and CVM teams from operating at the speed the business requires.

The Difference Between Knowing and Acting

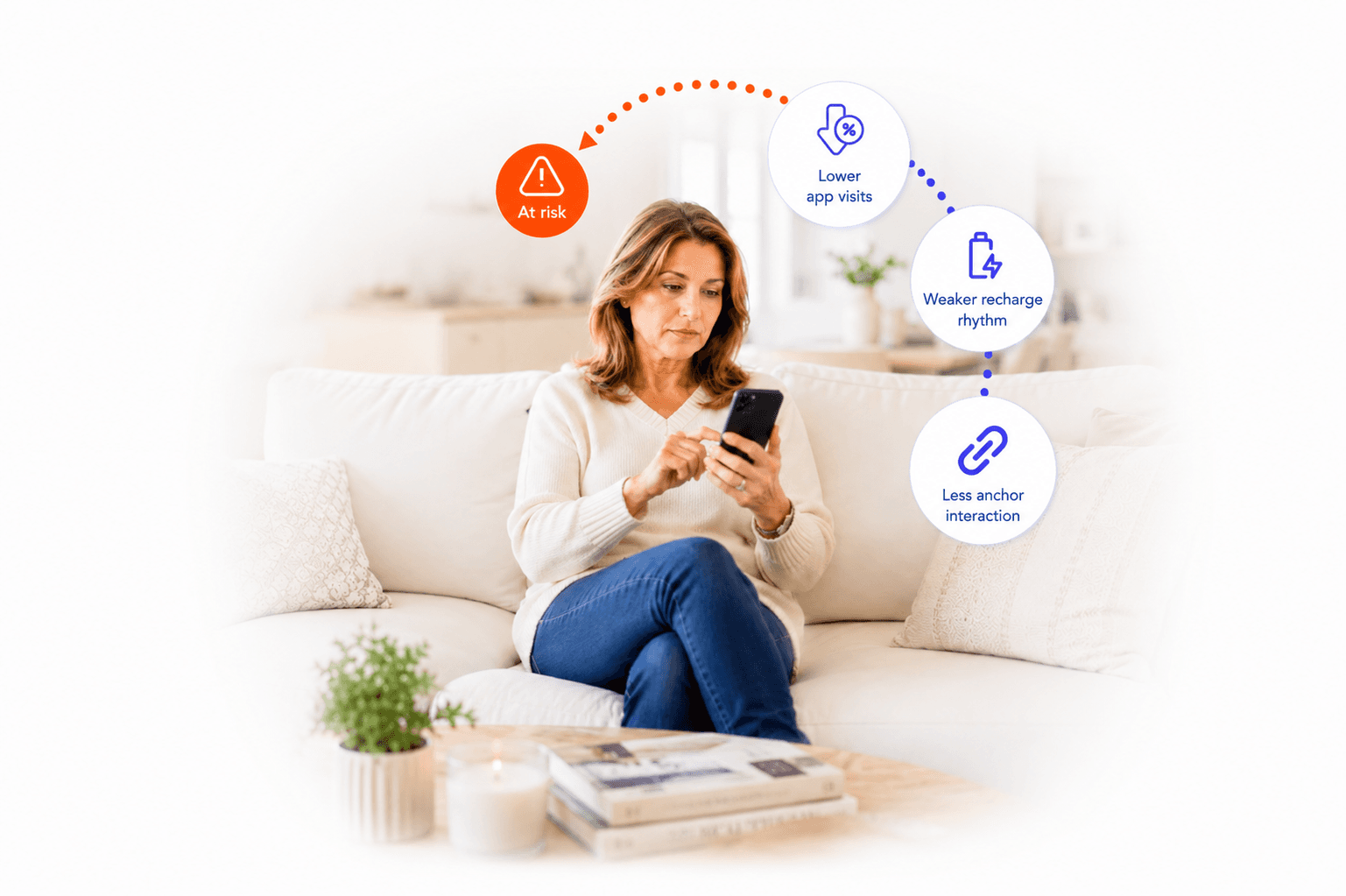

Banks that have invested in data infrastructure, predictive modeling, and customer analytics have largely solved the knowing problem. They understand their customers well. They can predict churn, estimate propensity, identify cross-sell opportunities, and model lifetime value with reasonable accuracy.

The gap that limits the return on these investments is not analytical. It is executional. The distance between detecting a customer signal and acting on it, in milliseconds, in the right channel, with the right offer, suppressed where appropriate, and consistent across every touchpoint, is where next best offer either delivers its promise or reduces to a more expensive version of the campaign scheduling it was meant to replace.

The architecture that closes this gap is not a feature. It is a design choice about what kind of system the bank is building: one that responds to customers in the moments they are present, or one that responds to segments in the windows the calendar allows.

How evamX Powers Next Best Offer in Banking

evamX is built on the event-driven architecture that real-time next best offer decisioning requires. Every interaction across core banking, card systems, mobile and web apps, ATM networks, IVR, and call center platforms is captured as a live event, with no data duplication, no batch lag, and no middleware layer introducing latency between signal and decision.

The NBX decisioning engine evaluates each event against live customer context in milliseconds, running eligibility checks, suppression filters, and priority scoring in a single decision cycle. The output is the next best offer for this specific customer, in this specific channel, at this specific moment, delivered immediately through whatever touchpoint the customer is using from a single omnichannel orchestration layer.

Cross-channel memory is native to the architecture. A rejection at the ATM suppresses the offer on mobile. A conversion in-app closes the journey in every other queue. Every channel reflects the same decision, because every channel connects to the same decisioning layer.

For marketing and CVM teams, Journey Designer provides a no-code environment for configuring offer logic: eligibility rules, suppression windows, priority scores, display zones, and channel sequences, without IT dependency. Offers can be simulated in real time before activation, and Evo AI continuously surfaces which journeys are converting and where adjustments will improve outcomes.

evamX connects to existing banking infrastructure without architectural disruption, through pre-built connectors and a zero-copy streaming layer that integrates with core banking systems, DWH and data lakes, CRM, card platforms, and third-party tools. Deployment is available on-premise, cloud, private cloud, or hybrid, aligned to the security and regulatory requirements of banking environments.

Request a Demo to see how evamX delivers next best offer decisioning at the moment it matters in banking.